Kenyan motorists are waking up to a frustrating new reality. After a network of smart cameras catches a driver speeding, they receive an SMS notification. The message is clear: they have committed an offence, and they have seven days to pay.

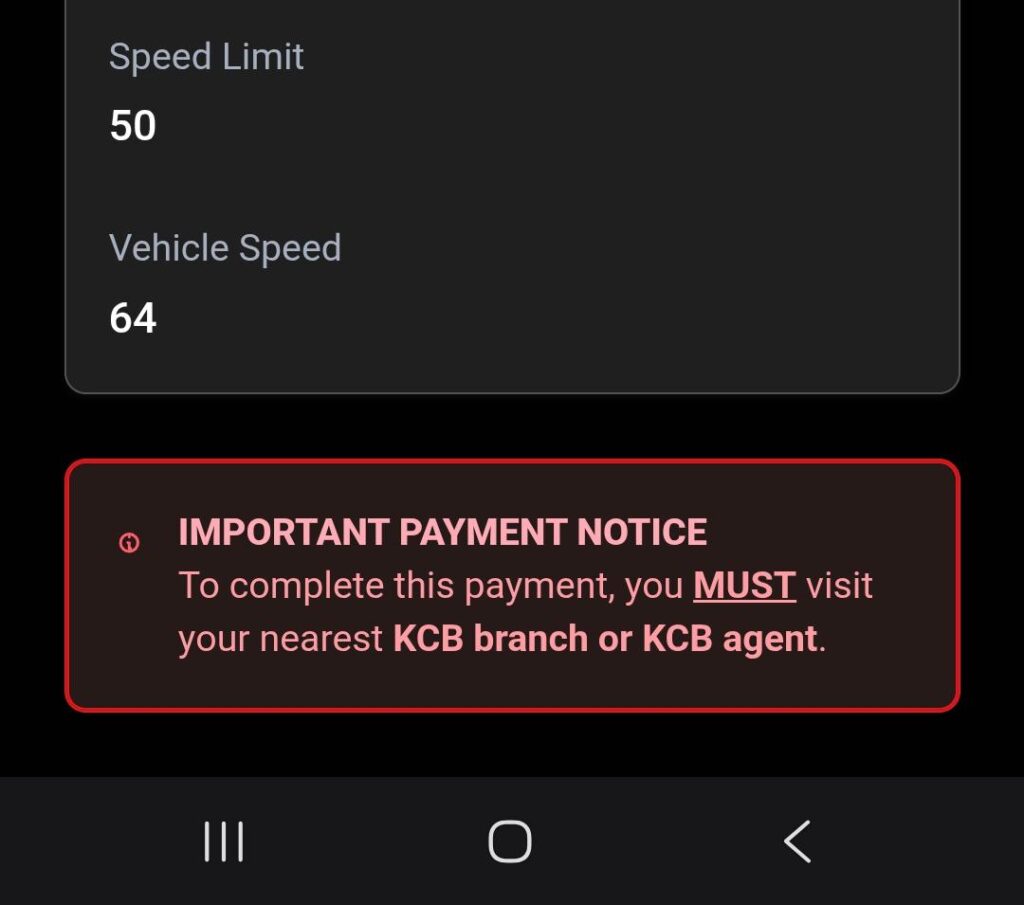

But here is the catch that is causing widespread anger and confusion. For now, motorists cannot simply use their phones to pay this fine. They are being forced to visit a KCB branch or agent in person.

This directive from the National Transport and Safety Authority (NTSA) has raised serious questions. In a country that pioneered mobile money and relies heavily on M-Pesa for daily transactions, why is the only way to pay an instant fine a physical visit to a bank?

The NTSA Director General, Nashon Kondiwa, has defended this decision, stating that it is a necessary step to protect motorists from fraudsters.

By restricting payments to KCB, the authority claims it is preventing criminals from sending fake messages with payment links and stealing money from unsuspecting Kenyans.While protecting the public from scams is a valid concern, this explanation does not hold water.

Why must the average Kenyan be inconvenienced by a long trip to a bank agent, which may even come with an extra service fee, simply because the government has not secured its own system?

The ban on M-Pesa payments seems less like a security measure and more like a move to force motorists into a specific banking channel. Many Kenyans are asking: why is KCB the only bank involved?

Why must everyone visit KCB? This has the appearance of a coercive arrangement that benefits a single institution at the expense of the public.

Looking deeper, the controversy goes far beyond mere convenience. Reports reveal that KCB is part of a consortium that has entered a lucrative 21-year public-private partnership (PPP) with NTSA. This deal will see the consortium invest billions of shillings in installing the smart cameras and smart driving licenses.

To recoup this massive investment, they will take a staggering cut from the traffic fines collected. The private investors are projected to receive over 77% of the revenue from this project, leaving the government with less than a quarter of the pie.

This arrangement creates a fundamental conflict of interest. The system is no longer just about making our roads safe; it has become a business venture designed to generate massive profits for private investors.

When the goal is to maximize revenue, the incentive is to catch as many offenders as possible, even for minor infractions that may not be a serious danger to road safety.

The decision to force payments through KCB ensures that this private partner gets its cut of the money as efficiently and exclusively as possible, turning the enforcement of traffic laws into a collection service for a private company.

Adding to the anger is the sheer unpredictability of the fines. In the example of a driver caught at 64 km/h, one must question the road conditions and the signage. Are these cameras placed fairly, or are they hidden in locations designed to trap drivers?

By presenting an automated fine with no immediate chance to challenge it and forcing a bank visit to pay, the NTSA is treating Kenyans like suspects who are guilty until they prove their innocence.

The system is automated, making it easy to issue a fine, but it has removed the human element of discretion, leaving motorists with no recourse but to pay.

This is not just about a 50 shilling M-Pesa fee; it is about principle.

The NTSA’s opaque partnership with KCB has corrupted what should be a public safety initiative into a scheme that feels more like extortion.

Motorists are left with a simple choice: make a special trip to KCB or face penalties and blocked services. This is not the digital future we were promised.

The government must reconsider this deal and allow Kenyans the simple freedom to pay their fines using the mobile money system they helped create.

Add Comment