The court has ordered Ngao Credit Limited to immediately release a client’s motor vehicle that it illegally repossessed, even after the client had already repaid KShs. 254,909 on a loan of just KShs. 120,000 – more than double the principal amount.

Despite these payments, the company continued demanding an additional KShs. 258,424.22 based on what the court found to be unlawful interest and penalty computations.

In its ruling, the court established that the client had a prima facie case, noting that the principal loan had been repaid nearly twice over.

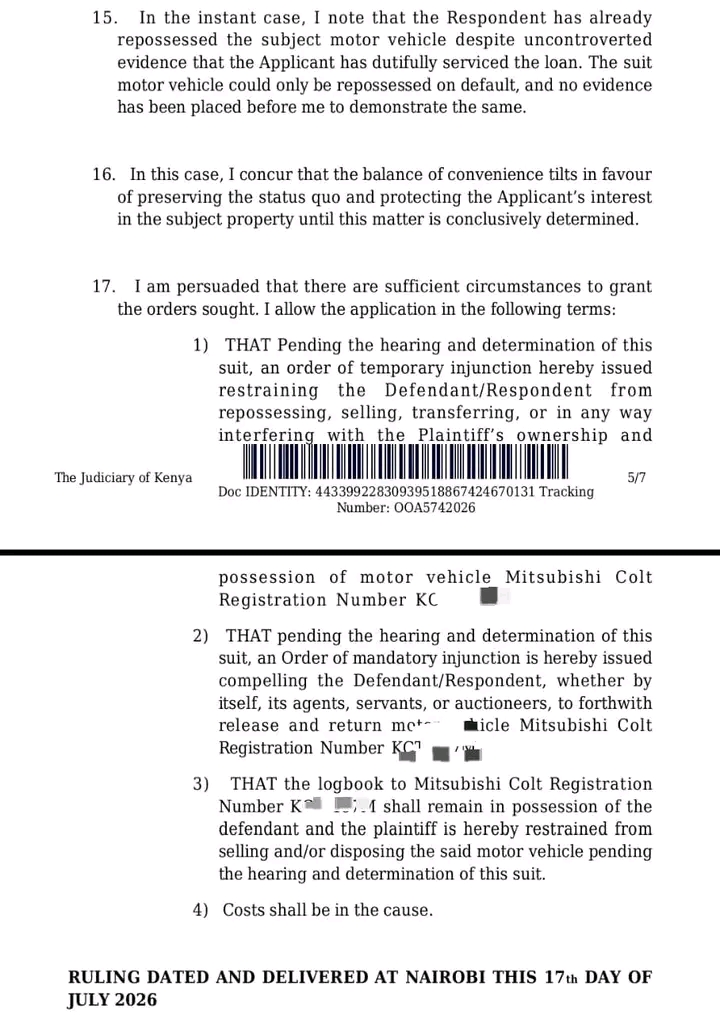

The court also pointed out that Ngao Credit failed to produce any evidence of default to justify repossessing the vehicle.

As a result, the court issued a mandatory injunction compelling Ngao Credit to release and return the motor vehicle, while also restraining it from repossessing, selling, transferring, or interfering with the vehicle in any way.

This ruling exposes a troubling pattern in the microfinance sector. Here was a borrower who took a small loan and paid back more than double the amount, yet the lender still came after them for more money and took their vehicle without legal justification.

This is not an isolated incident. Many Kenyans have found themselves in similar situations, taking small loans only to be crushed by interest rates and penalties that seem to have no end.

The numbers in this case tell the story clearly: borrowing KShs. 120,000 and repaying KShs. 254,909 should be the end of the matter, not the beginning of more demands.

What makes this case particularly significant is the court’s observation that Ngao Credit could not produce any evidence of default.

This means the company acted without proof that the borrower had broken the agreement. They simply took the vehicle based on their own calculations and demands.

This kind of behavior is unacceptable in a country governed by laws that protect citizens from arbitrary actions by powerful institutions. The court stepped in to correct this overreach, and their decision should give hope to other borrowers who might be facing similar treatment.

The mandatory injunction issued by the court is a strong remedy. It does not just tell Ngao Credit to stop what they are doing; it forces them to take positive action to return what they took.

This type of court order is not given lightly, and its issuance shows the strength of the borrower’s case. The court essentially determined that the borrower’s right to their property was being violated and that immediate intervention was necessary to prevent further harm.

For Ngao Credit, this ruling is a serious blow to their business practices. They now have a court decision publicly confirming that they demanded money unlawfully and repossessed a vehicle without justification.

Such rulings can damage a company’s reputation and make potential customers think twice before entering into agreements with them.

The company will also have to bear the costs and inconvenience of returning the vehicle and potentially facing further legal consequences.

For borrowers, this case offers important lessons. First, it shows that courts are willing to protect consumers against predatory lending practices.

Second, it demonstrates the importance of keeping records of all payments made. In this case, the borrower was able to prove that they had repaid more than double the principal amount, which was crucial evidence in court.

Third, it shows that borrowers should not simply accept demands from lenders without questioning them. If a lender is asking for amounts that seem unreasonable, it is worth seeking legal advice.

Add Comment