Kenya’s financial sector is now facing new concerns as even licensed banks begin using tactics that were once associated only with rogue digital lenders. Cyprian Is Nyakundi, a consistent critic of privacy violations in the lending industry, has exposed a disturbing case involving Absa Bank Kenya.

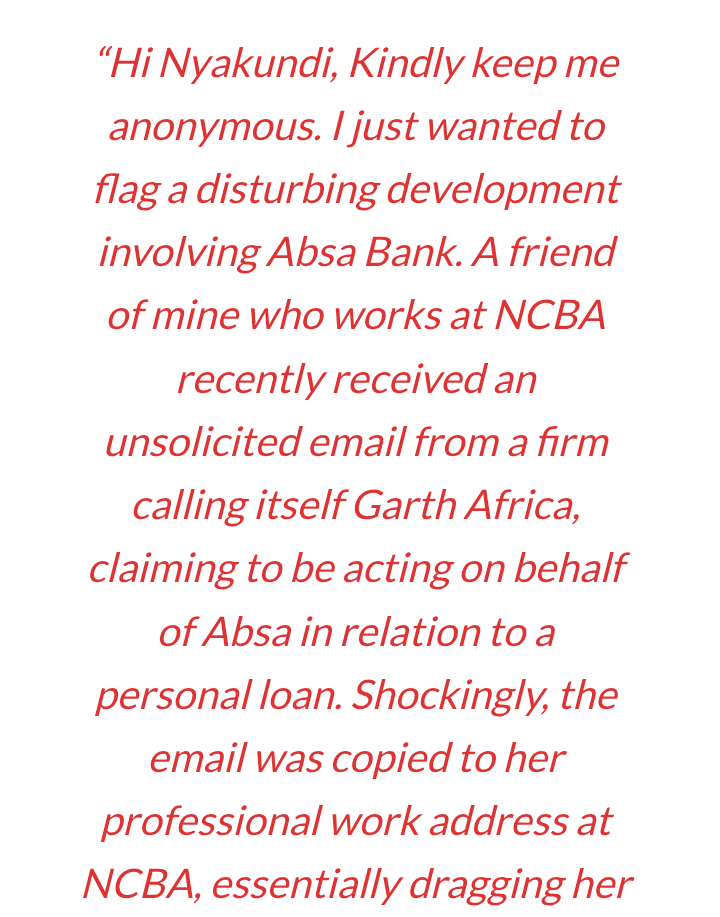

Through a source who reached out to him anonymously, Nyakundi shared how a staff member at NCBA Bank received an unsolicited email from a firm called Garth Africa, which claimed to be working on behalf of Absa.

The email not only revealed sensitive loan information but was also copied to the employee’s official NCBA work email, pulling her employer into a private financial matter without her approval.

This incident mirrors what loan apps like Truepesa, Fairkash, Okash, and others have been known to do contacting people in a borrower’s phonebook to shame them into repaying.

For a licensed bank to adopt such humiliating and intrusive methods raises serious concerns about the breakdown of professional standards in the banking sector.

The sender of the email seemed to rely on public embarrassment as a tool to pressure the borrower, a move that undermines customer trust and violates basic data privacy norms.

What makes this worse is that it wasn’t Absa directly reaching out but a third-party agent, allowing the bank to possibly dodge direct responsibility.

This tactic is not only deceptive but also raises questions about data handling and oversight within established banks. If a major institution like Absa is comfortable using such backdoor methods, what does that mean for customers who trust banks with their most sensitive information?

The lack of strong action from regulators like the Central Bank of Kenya and the Office of the Data Protection Commissioner is also worrying.

These agencies are meant to shield citizens from such abuse, yet incidents like this continue to go unchecked. Allowing banks to contract aggressive third parties without accountability could lead to more cases where borrowers are publicly shamed, professionally embarrassed, or exposed to unnecessary pressure.

This is no longer about just collecting money. It is about how institutions are now using people’s personal lives and workplaces as weapons in loan recovery.

Such behavior needs immediate attention from regulators and stronger protection for borrowers. Nyakundi’s exposure of this case has opened the door to a wider investigation into whether such incidents are isolated or part of a growing pattern within Kenya’s banking system.

More victims are encouraged to speak out so that this growing misuse of power can be addressed before it becomes the new normal.

Add Comment