Cyprian Nyakundi shared on his X page a concerning update about the state of Kenya’s debt under President William Ruto’s administration. According to the National Treasury, between September and December 2024, the government borrowed Ksh 572 million every single day, which adds up to Ksh 68.7 billion in new loans in just four months.

These loans come from both bilateral and commercial lenders, including 15 loans from the China Development Bank, as well as additional funding from countries like Italy, Germany, and France.

The interest rates on these loans vary, ranging from 0.25% to 4%. However, it’s important to note that some of these loans have extra fees, including commitment and upfront charges, which will increase the total amount Kenya owes.

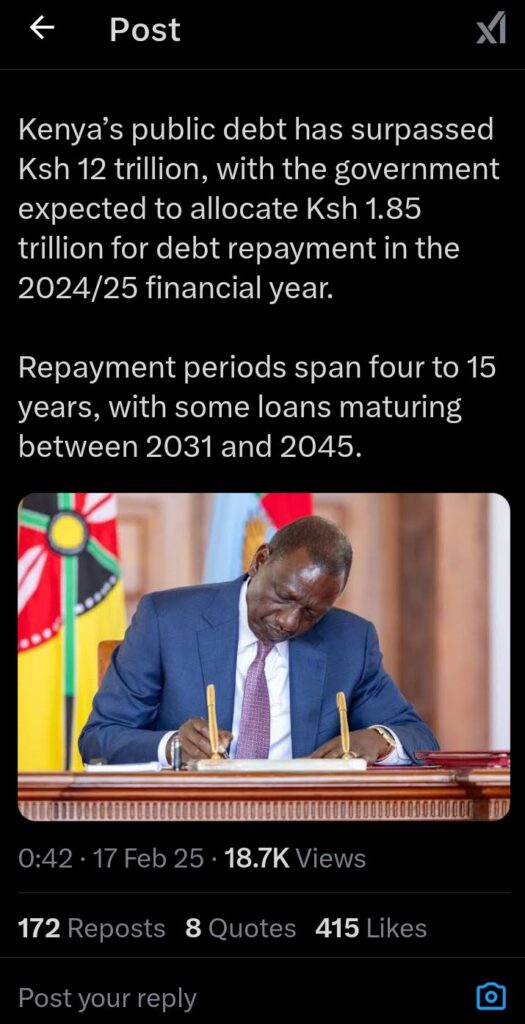

The country’s public debt has now crossed Ksh 12 trillion, a huge figure that continues to grow at an alarming rate. In the 2024/25 financial year, the government has set aside Ksh 1.85 trillion just to repay its debts.

This is a large portion of the national budget, and it means there will be less money available for important services like health care, education, and infrastructure.

The repayment period for the loans is long, with some stretching between four to 15 years. Some loans will not mature until as late as 2045, which means future governments will have to continue paying off debts that were taken out by the current administration.

This puts a heavy financial burden on future generations. Many people are concerned that this growing debt could lead to economic problems down the line. If the government keeps borrowing at this rate, it could find itself unable to repay its loans, leading to higher interest rates and stricter terms on future borrowing.

There’s also growing frustration among Kenyans about the way the government is handling its finances. While the government claims it is borrowing for development purposes, many citizens feel that they are not seeing enough results. Infrastructure projects and public services should be improving with all this borrowing, but the reality is that many people are still struggling with high living costs and poor services.

This makes it difficult for many to understand why the government is taking on more loans instead of using its resources to solve pressing issues.

Cyprian Nyakundi’s post highlights a deeper concern, the lack of transparency in how borrowed funds are being used. With such a large amount of debt, it’s critical that the government provides clear answers about how these loans are being spent. If funds are not used effectively, Kenya could find itself in a dangerous financial situation.

Borrowing should ideally lead to real improvements in the country’s economy, but without clear results, it risks leading to a never-ending cycle of debt.

The growing national debt has raised serious questions about Kenya’s financial future. If the government does not take steps to reduce borrowing and use funds more effectively, the country could face long-term financial instability. The current borrowing patterns are unsustainable and could harm the economy for years to come.

Add Comment