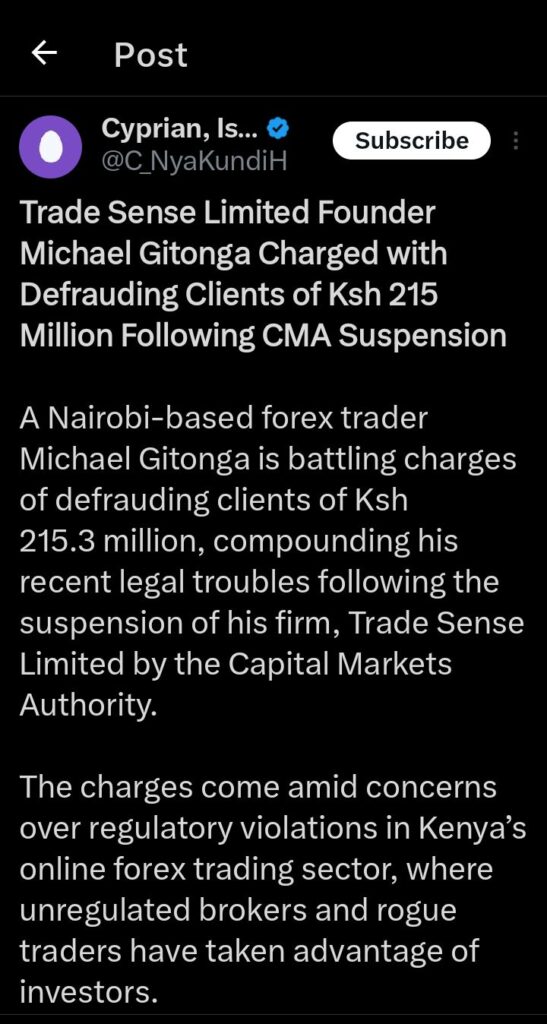

Cyprian Is Nyakundi shared on his X handle about the case of Michael Gitonga, the founder of Trade Sense Limited, who has been charged with defrauding clients of Ksh 215 million. This case has raised serious concerns about the state of Kenya’s forex trading sector and how rogue traders take advantage of investors.

Gitonga’s company was recently suspended by the Capital Markets Authority (CMA) over governance and financial compliance issues, but his troubles did not end there. He now faces accusations of illegally handling client funds and diverting them for personal use.

According to court documents, Gitonga, also known as Tosh, allegedly took Ksh 212.16 million from clients between April 2022 and August 2024.

The money was supposed to be invested in forex trading, but he reportedly misused it. On top of that, he is accused of fraudulently obtaining Ksh 3.14 million from three individuals under false pretenses.

Kenya’s forex trading laws clearly state that money managers cannot access client funds directly, yet Gitonga allegedly ignored this rule. Instead of guiding clients on how to invest, he took control of their funds, raising suspicions of fraud.

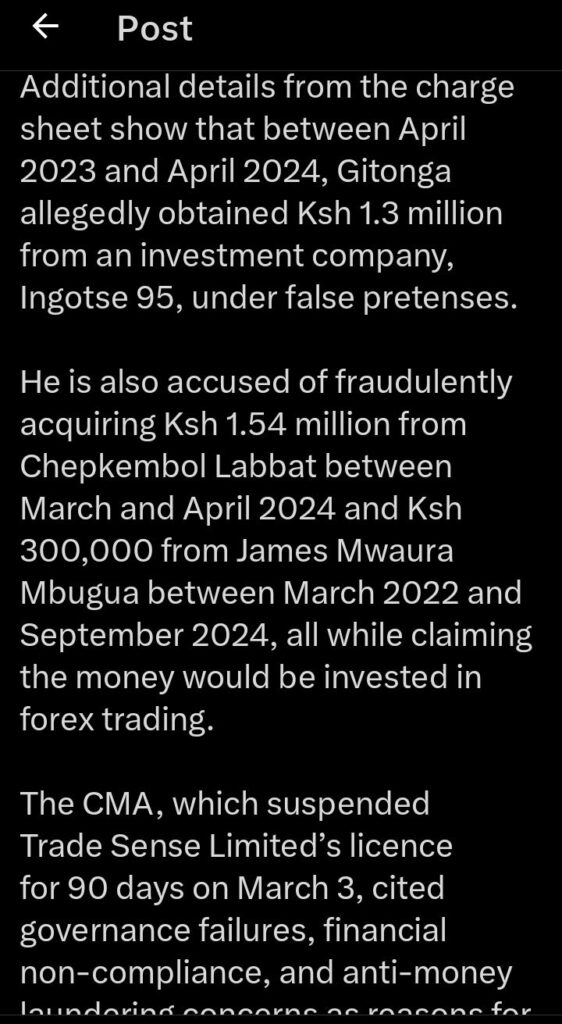

The charge sheet also reveals more details about how Gitonga allegedly conducted his scheme. Between April 2023 and April 2024, he is said to have obtained Ksh 1.3 million from an investment company, Ingotse 95, by making false promises.

Another investor, Chepkembol Labbat, allegedly lost Ksh 1.54 million to Gitonga between March and April 2024. James Mwaura Mbugua also claims to have lost Ksh 300,000 between March 2022 and September 2024, all based on Gitonga’s promise to invest the funds in forex trading. These accusations paint a picture of a trader who used deception to collect millions from unsuspecting investors.

CMA’s decision to suspend Trade Sense Limited came on March 3, citing financial non-compliance and concerns over anti-money laundering practices. The regulator had been monitoring the company since 2023, which suggests that Gitonga had been under scrutiny for some time.

His company required clients to invest a minimum of Ksh 258,380 for retail accounts and Ksh 1.2 million for corporate investors. There was also a 90-day lock-in period for the initial investment, along with a three percent management fee charged daily.

Such terms might have looked professional on the surface, but with the current charges, many now question whether the entire setup was designed to exploit investors.Kenya’s forex market has attracted many investors in recent years, but it has also become a hotbed for fraud.

CMA only licenses non-dealing brokers, meaning they cannot trade for clients but can only provide trading platforms. However, some traders have found loopholes to operate as if they have full control over client funds.

This has led to massive losses for investors who are often lured with promises of quick and high returns. The forex market itself is worth over $7.5 trillion globally, making it one of the most lucrative financial sectors. But without strict enforcement, fraud cases like Gitonga’s are bound to continue.

Regulators in Kenya introduced the Online Foreign Exchange Trading Regulations in 2017 to protect investors, but enforcement remains a challenge. Many traders still operate outside the law, deceiving people with promises of guaranteed profits.

Gitonga’s case is now a major test for CMA and the judiciary. If he is found guilty, it could send a strong message to other rogue traders. CMA has given itself 90 days to decide whether to lift or extend Trade Sense Limited’s suspension, or if more action is needed. Investors, meanwhile, will be watching closely to see if justice is served in this case.

Add Comment